An assortment of code snippet collections and useful code blocks that I have applied to various projects.

Classification algorithm comparisons

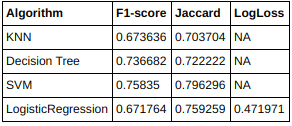

Algorithm comparison on finance loans

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

| algo_result = pd.DataFrame(columns=['Algorithm', 'F1-score', 'Jaccard', 'LogLoss']) | |

| algos = ["KNN","Decision Tree","SVM", "LogisticRegression"] | |

| for algo in algos: | |

| if algo == 'KNN': | |

| yhat=clf.predict(test_X) | |

| log_val = 'NA' | |

| if algo == 'Decision Tree': | |

| yhat= loanTree.predict(test_X) #Running the Decision Tree evaluation metrics | |

| log_val = 'NA' | |

| if algo == 'SVM': | |

| yhat= loanS.predict(test_X) #Running the SVM evaluation metrics | |

| log_val = 'NA' | |

| if algo == 'LogisticRegression': | |

| yhat= LR.predict(test_X) #Running the LogisticRegression evaluation metrics | |

| log_val = log_loss(test_y, LR.predict_proba(test_X)) | |

| algo_result = algo_result.append({'Algorithm': algo, | |

| 'Jaccard': jaccard_similarity_score(test_y, yhat), | |

| 'F1-score': f1_score(test_y, yhat, average='weighted'), | |

| 'LogLoss': log_val}, ignore_index=True) | |

| algo_result.style.hide_index() |

The output of the above code shows a table of algorithm comparisons where the support vector machine(SVM) yielded the best result.

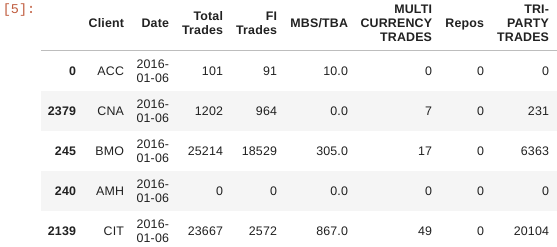

Resample and Summarize Time Series Data With Pandas – Daily to Weekly Summary

Example of resampling daily trading activity into weekly in order to later perform a comparison against a separate dataset which is only collected on Wednesdays.

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

| #convert daily data to weekly for each client | |

| weekly_trades = FT_volumes.groupby("Client").resample('W-Wed', | |

| label='right', closed = 'right', on='Date').sum().reset_index().sort_values(by='Date') | |

| weekly_trades.reset_index(inplace=True) | |

| weekly_trades.head() |